121M+Total Funded

Entry from $10–$100 vs $1,000+ for many funds

What you gain, what you risk, and who this model works best for

Lower minimums and direct access, but also higher risk and less liquidity than conventional investment vehicles

Entry from $10–$100 vs $1,000+ for many funds

Direct project choice instead of fund manager decisions

Lock-in periods often 1–5 years

Default rates vary 2–15% depending on sector

No secondary market on most platforms

Investors who received at least one interest payment each month.

Rated 4.5 / 5 based on 779 reviews. Showing our 4 & 5 star reviews.

From campaign launch to payout, what happens at each stage

Due diligence varies widely; some platforms check financials, others run light verification only

Investors review terms, ask questions, and commit funds during a fixed campaign period

If the goal isn't hit, funds return to investors; if met, the project moves forward

Platform releases funds to the borrower or business after deducting fees

Investors receive interest or dividends on schedule, assuming the project performs as expected

At maturity, you get principal back or face partial loss if the borrower defaults

Access, control, diversification, and the chance to back projects banks won't touch

No fees for deposits, investments or withdrawals.

A growing community built around transparent investing.

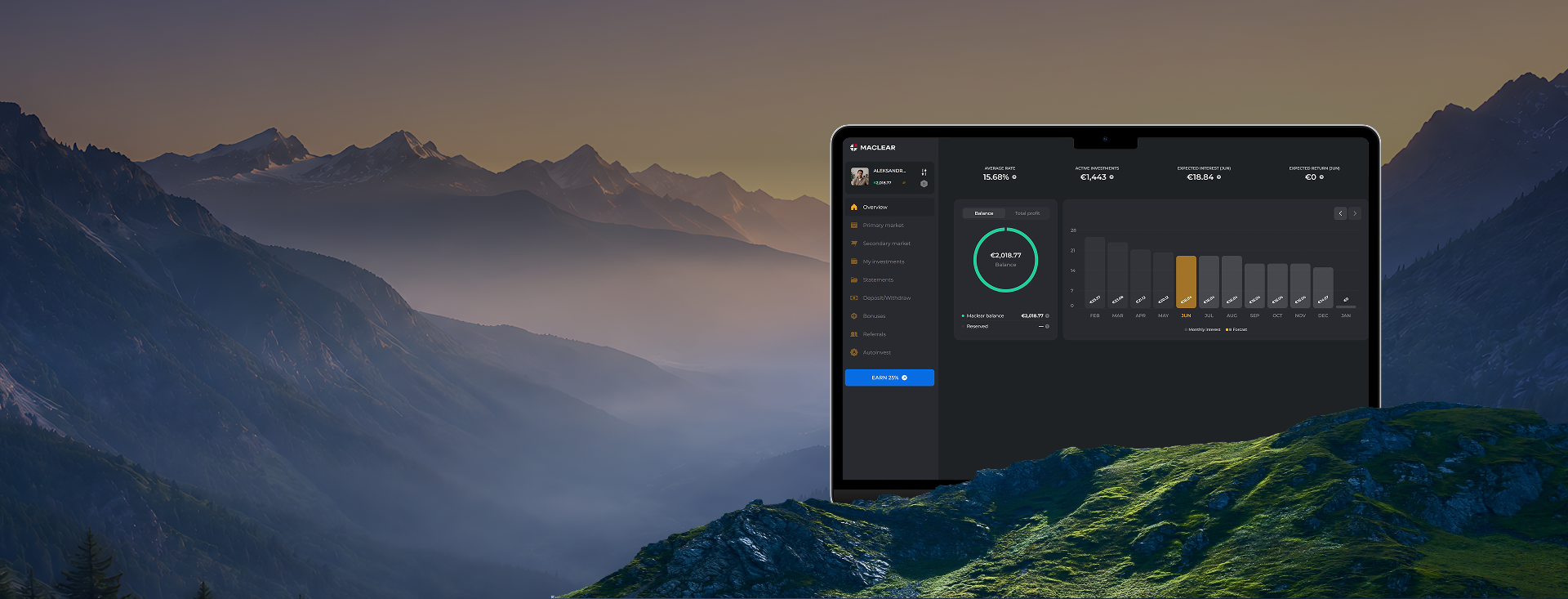

Average amount invested by active users each month.

Average interest paid to active investors each month.

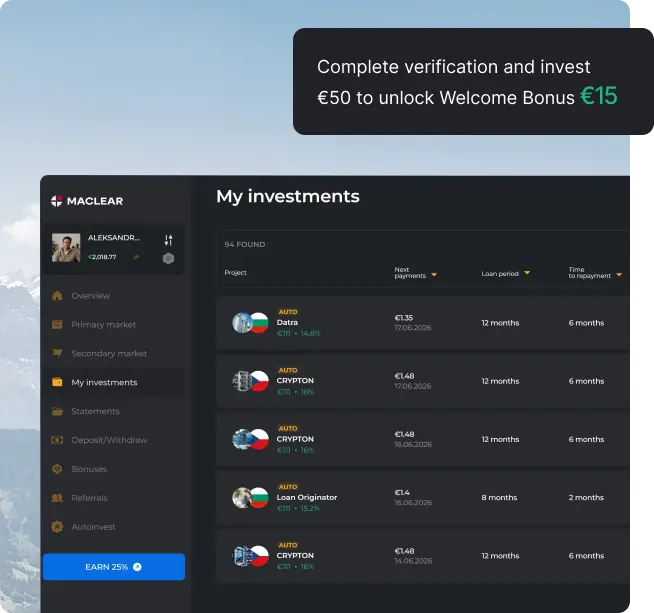

Vetted projects currently open for funding across real estate, business loans, and renewable energy

Supplies consumer electronics to major retailers and telecomes like Technomarket and Magnum-D

Processes, freezes and dries fruits and vegetables in a modern, fully equipped organic-focused production facility

Supply, installation and maintenance of agricultural and food equipment

Average annual return17.6%

Earned return€460

Promotions€0

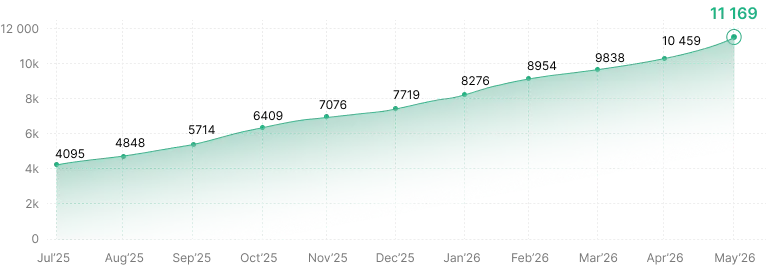

Estimated returns based on target rate of 14.6% APY. Actual returns may vary. Past performance does not guarantee future results.

And what you can't, no matter which platform you use

You choose where your money goes and can skip anything that doesn't fit your risk appetite

You decide how many projects to fund and how much to allocate to each sector or risk grade

Most platforms lock funds until maturity; secondary markets exist but often have low liquidity

You can't control whether a business hits revenue targets or a property sells on schedule

If the platform shuts down, accessing your investments can become complicated or impossible

New rules can affect tax treatment, platform operations, or investor protections without warning

Recessions, interest rate shifts, or sector downturns impact repayment rates across your portfolio

Borrowers know more about their financials than you do, even after platform due diligence

Filter by sector, term length, expected return, and risk grade to find opportunities that match your strategy

Explore projects

Higher advertised returns often signal higher default risk; platforms with the best track records tend to sit in the middle

Conservative projects: 3–6% annual return

High-risk projects: 10–15%+ if repaid

From account setup to first investment in three steps

Identity verification required

Bank transfer or card

Start small and diversify

Some platforms reward repeat investors with fee discounts or early access to high-demand projects

Lower platform commission

Before public launch

Extra 0.25–0.5% APY

Earn when friends invest

Direct investment in deals traditional banks reject, featuring easier access but greater risk and minimal regulation compared to conventional options. Ideal for those comfortable with potential losses who desire control over capital allocation.

Disclosure quality varies. The best platforms publish default rates, borrower financials, and audit reports. Others share minimal data, making it hard to assess true risk. Always check what information you'll get before and after investing, and whether past performance metrics are independently verified.

![]() Collateral and the

Provision Fund help reduce certain risks, but do not eliminate investment risk.

Collateral and the

Provision Fund help reduce certain risks, but do not eliminate investment risk.

Crowdfunding platforms typically accept investments starting at $10–$100 per project, compared to $1,000+ minimums for traditional mutual funds and institutional vehicles. This accessibility allows retail investors to build diversified portfolios across multiple opportunities without substantial upfront capital.

Most crowdfunding investments have lock-in periods ranging from 1 to 5 years, during which investors cannot access or sell their positions. This illiquidity differs sharply from stock markets, where secondary trading provides exit flexibility.

Historical default rates on crowdfunding platforms vary between 2% and 15% depending on the sector and borrower profile. Real estate and established business ventures typically carry lower risk, while early-stage startups present higher probability of non-repayment.

Platform screening filters out obviously fraudulent or unviable proposals before campaigns go live. However, due diligence depth varies significantly—some operators conduct thorough financial audits while others perform only cursory background checks.

Most P2P lending and equity crowdfunding platforms lack secondary markets, meaning investors cannot sell stakes to other buyers before the funding period closes. This distinguishes crowdfunding from traditional public securities with active trading infrastructure.